You closed three jobs last month. You sent the invoices. Revenue is up from last quarter. And yet — you're checking your bank balance at 11pm on a Sunday, stomach tight, wondering how you're going to cover payroll, a supplier invoice, and a tax deposit all hitting in the same week.

This isn't a revenue problem. It's a cash flow problem. And it's killing small businesses every day — not because the owners aren't working hard or don't have customers, but because nobody taught them how money actually moves through a business.

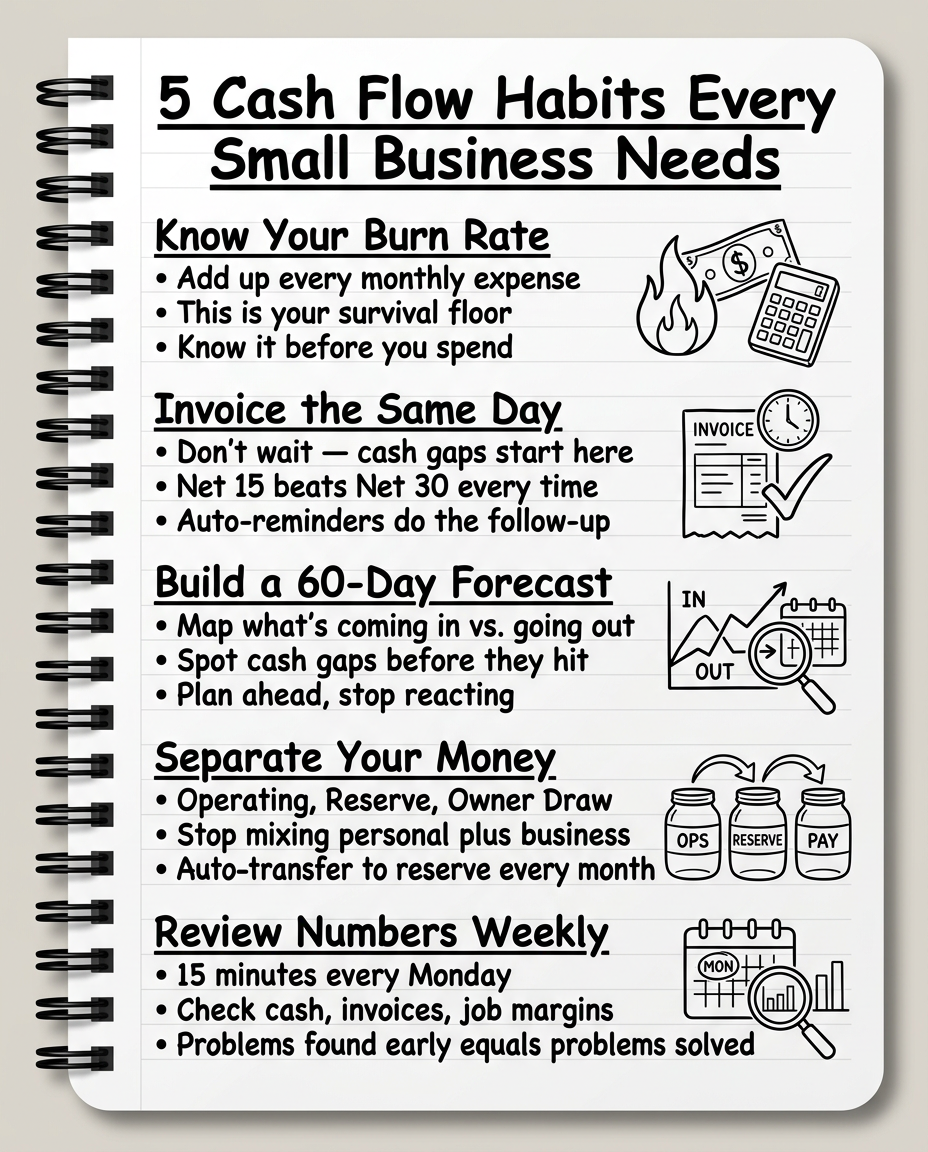

This post is for you if you're in the RUN stage — your business is open, customers are coming in, but the financial side feels like you're flying blind. Here are 5 cash flow habits that will change how you operate, starting this week.

Habit 1: Know Your Real Number — What It Costs You to Open Your Doors Each Month

Most business owners know their revenue. Very few know their actual monthly burn. Your burn rate is the minimum amount of money your business needs to spend just to stay operational — before you make a single dollar of profit. Rent, software, insurance, payroll, loan payments, vehicle costs, fuel, every recurring expense that hits whether you have one job booked or twenty.

Here's why this matters: if you don't know your burn, you can't know whether a good month is actually good. You might gross $18,000 and feel great — until you realize your burn is $16,500 and you netted $1,500. After taxes, you made nothing. Worse, if next month is slow and you only gross $12,000, you're $4,500 in the hole before you pay yourself a dollar.

How to build it

Pull the last 3 months of bank and credit card statements. List every single recurring expense and group into:

- • Fixed — same every month (rent, insurance, subscriptions)

- • Variable Fixed — fluctuate but always present (fuel, supplies, utilities)

- • Owner Draw — what you pay yourself

Add them up. That's your baseline burn. Anything above it is real margin. Anything below it is a deficit.

CogniFlow Books can categorize and track these expenses automatically so you're not doing this math manually every month. Your burn rate becomes a live number, not a guessing game.

Action step

This week, calculate your burn rate. Write the number down. Post it somewhere visible. This is your floor — every business decision you make should start here.

Habit 2: Invoice Fast, Follow Up Faster — Cash Doesn't Come in by Itself

Here's a pattern that plays out constantly in service businesses: the job gets done, the owner puts off sending the invoice because they're already on the next job, the invoice goes out 5 days late, the client waits 30 days to pay, and suddenly you're 35 days past completion with nothing in the bank. Multiply that by 4–6 open jobs at a time and you're looking at a serious cash gap — even if every client eventually pays in full.

The fix requires discipline: invoice the same day the job is complete. Not tomorrow. That day. If possible, collect a deposit upfront and a final payment at completion, before you pack your tools.

Follow-up sequence

Day 1: Invoice sent — Net 15, not Net 30

Day 16: Friendly reminder — "following up on invoice #104..."

Day 23: Firmer follow-up — "now 8 days past due..."

Day 30+: Phone call, then late fee if contract allows

Most clients aren't trying to stiff you — they're busy and paying whoever is loudest. Be the loudest. Automated invoice reminders built into platforms like CogniFlow Books send those follow-ups on a schedule so you're chasing cash without spending time chasing cash.

Action step

Look at your open invoices right now. If any are past due, send a follow-up today. Then set a rule: invoices go out within 24 hours of job completion, no exceptions.

Habit 3: Build a 60-Day Cash Forecast — Stop Reacting, Start Predicting

“I have enough money right now” is not a cash flow strategy. Cash flow management is about the future — knowing what's coming in and what's going out over the next 30, 60, and 90 days.

Column A — Cash In

- • Outstanding invoices + due dates

- • Booked jobs and expected revenue

- • Recurring revenue (retainers, contracts)

Column B — Cash Out

- • Bills due in the next 60 days

- • Payroll, taxes, loan payments

- • Supplier invoices, renewals

Subtract B from A, week by week. What you're looking for are cash gaps — weeks where outflows exceed inflows. If you find one, you have time to act: speed up a collection, delay a purchase, draw on a line of credit, or proactively reach out to a client about early payment.

Most business owners only discover cash gaps when they're already in them. By then, you're reacting with panic instead of responding with a plan.

Action step

Build a basic 60-day cash forecast this week. Even a rough one. List what you expect to collect and what you know is going out. Circle any red weeks — that's where your attention needs to go.

Habit 4: Separate Your Money — Operating, Reserve, and Owner Draw

You'd be surprised how many business owners in year 2, 3, even year 5 are still running everything through one account — personal and business money mixed together. When that happens: you can't tell if the business is actually profitable, you spend business money on personal things without realizing the impact, and there's never a reserve built up because “extra” money disappears into daily spending.

Account 1 — Business Operating

All revenue comes in here. All business expenses go out from here. Nothing personal touches this account.

Account 2 — Business Reserve

Every time revenue hits operating, automatically transfer a percentage here. Start at 5–10%. Work toward 3–6 months of burn.

Account 3 — Owner Draw / Personal

Pay yourself a consistent amount from operating on a set schedule. This is what you live on. Stop dipping into operating randomly.

Your reserve account is not savings. It is not vacation money. It is the buffer that keeps your business alive when the unexpected happens.

Action step

If you don't have this three-account structure, open the accounts this week. Most business banks allow multiple accounts under one entity at no cost. Set up an auto-transfer of even 5% of every deposit into reserve. Start small. Start now.

Habit 5: Review Your Numbers Weekly — Not Monthly, Not Quarterly, Weekly

Most small business owners ignore their financials all month, hand a shoebox of receipts to their accountant, and find out how the quarter went 45 days after it ended. By then, the decisions that would have mattered have already been made — or missed.

Cash flow management requires current information. A 15-minute weekly numbers check can tell you:

- • How much cash is in each account right now

- • What invoices are outstanding and which are overdue

- • What's due to go out this week

- • Whether you're trending ahead or behind your 60-day forecast

- • Whether any job came in under margin

That last point — job-level profitability— is one of the most overlooked numbers in a service business. You might be busy all month and still lose money if you're consistently underpricing or overrunning costs. Over time, patterns emerge: certain job types are always over budget, certain clients always create extra work. This information is pure gold — but only if you're tracking it.

If you're still doing this in spreadsheets or not at all, CogniFlow Books is built exactly for this — giving you a clear view of your cash, your jobs, and your margins without requiring you to become an accountant.

Action step

Block 15 minutes every Monday morning for your weekly numbers check. Check bank balances, review open invoices, look at what's going out this week, and scan your job margins from last week. Make it non-negotiable.

The Bigger Picture: Systems Beat Willpower Every Time

Most of these habits fail not because owners don't care, but because they rely on willpower and memory. You're busy — doing the work, selling the next job, managing your team, handling customer calls — and the financial admin keeps getting pushed to “later.”

Later is where businesses die.

The owners who build real financial stability have systems that do the work for them: automated invoicing, automatic reserve transfers, real-time dashboards, alerts when something's off. That's the difference between a business owner who knows their numbers and one who finds out too late.

This Week: Pick One and Start

Don't try to tackle all 5 at once. Pick the one that addresses your biggest current pain point.

If cash is unpredictable

Build your 60-day cash forecast. Pull the numbers, map the inflows and outflows, and find the gaps before they hit you.

If clients are slow to pay

Look at your open invoices today. Send the follow-ups that are overdue. Then set a rule — invoices go out within 24 hours of job completion.

If you don't know your real costs

Calculate your monthly burn rate this week. Add up every recurring expense and know your floor.

If your money is mixed

Open separate business accounts and set up an automatic reserve transfer, even if it's just 5% to start.

If you're not looking at your numbers

Block 15 minutes every Monday. Start this Monday.

Stop Managing Cash Flow Manually

CogniFlow Books is built for contractors, service businesses, and local business owners who want to track their money, run profitable jobs, and stop doing bookkeeping by hand. Job costs, invoicing, automated reminders, cash flow forecasting — all in one place. Try it free for 7 days.

Start Free Trial