If you're honest — how many bad weeks would it take before you're stressing over payroll, rent, or your own paycheck?

Experts recommend 3–6 months of operating expenses in cash reserves, but the median small business sits at just over 2 months — and many are running with far less. That means one slow quarter, one surprise bill, or one big client leaving can shove you into panic mode. You don't feel it when things are going well. You feel it when:

- • A job gets delayed

- • A customer pays late

- • A piece of equipment dies

- • A project falls through

- • A season hits harder than expected

Then suddenly you're moving money, swiping cards, delaying payments, and wondering why the business you built for freedom now feels like a trap. This post will show you how a cash cushion really works, how big yours should be, and how to build it without starving the business.

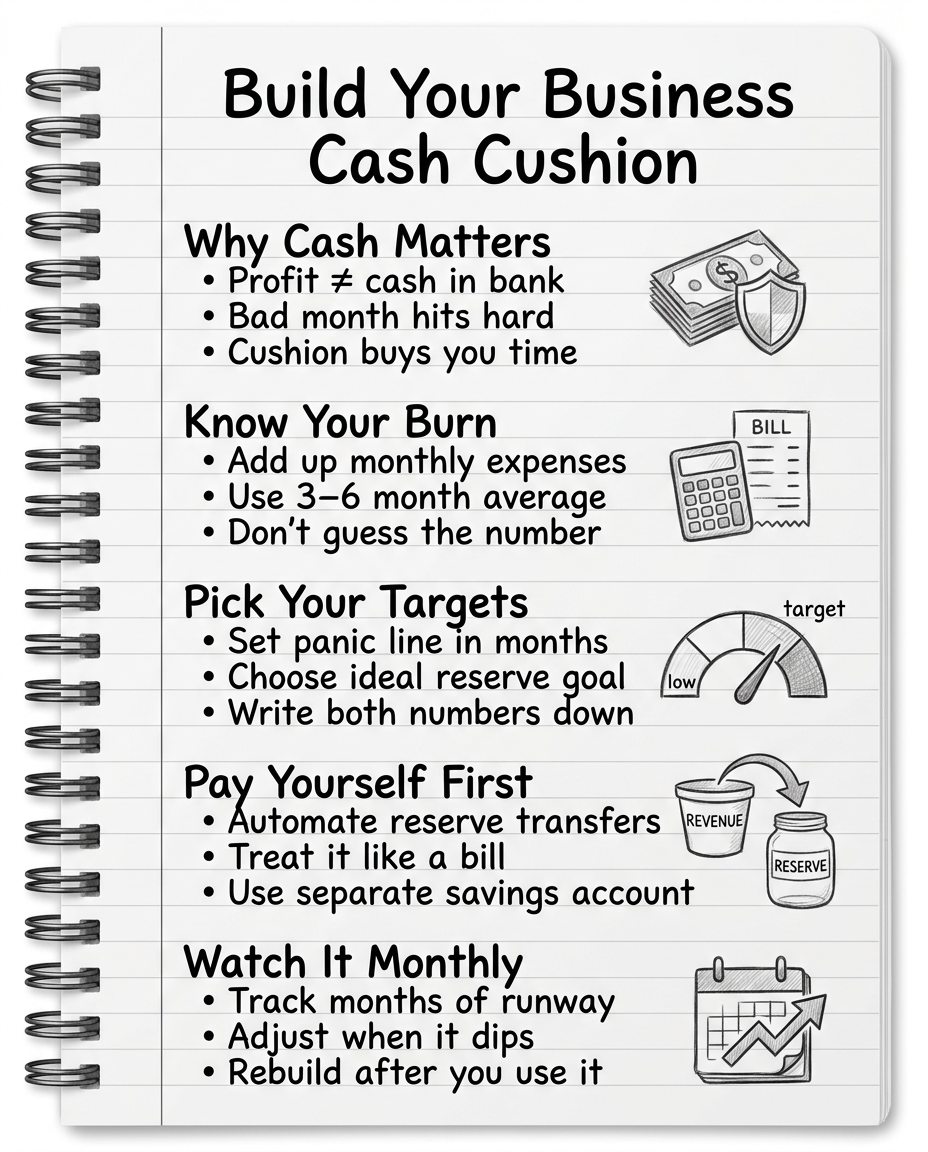

Why Cash Reserves Matter More Than Profit

Profit is what's left on paper after income and expenses. Cash is what's actually in your account when the bills hit.

You can be profitable and still run out of cash if customers pay slowly, you carry inventory, you front materials or labor, or you get hit with seasonal swings. That's why 72% of small business failures cite cash flow problems as a primary cause — not bad product, not no demand. Cash.

A cash reserve is simply a buffer between real life and your operating expenses. It lets you:

- • Survive a dry spell without nuking your personal savings

- • Take advantage of opportunities (equipment, a good hire, a new location) without scrambling

- • Sleep at night knowing one mistake won't wipe you out

The bigger your fixed costs, seasonality, or dependence on a few key customers, the closer you want to be to the upper end of the 3–6 month range. Being one bad month away from panic means growing on a weak foundation. Your reserve is the foundation.

How Big Should Your Cash Cushion Be?

Your ideal reserve depends on stage, revenue stability, cost volatility, and credit access. Here are simple targets:

You need two numbers — not a vague goal:

Panic Line

The minimum you refuse to go below. When you hit this, cut spending and aggressively chase receivables.

Target Reserve

The level where you feel safe making strategic decisions again. Build toward this.

Monthly operating expenses: $15,000

Panic line (2 months): $30,000

Target reserve (4 months): $60,000

Operating expenses include rent, payroll, utilities, software, insurance, vehicle costs, marketing, and any other recurring obligations. Not vibes — math.

The Real Reason You Don't Have a Reserve Yet

It's not because you're bad with money. It's because:

- • You treat “what's in the account right now” as free to spend

- • You haven't decided that reserves are a bill, not an optional nice-to-have

- • Your bookkeeping is messy, so you don't really trust your numbers

- • You're reacting, not planning

Most owners see $17k in the account and think “I can spend some of that.” Then taxes hit. Then a slow month hits. Then an emergency hits. And your “extra” money was never extra.

Owners who build reserves do it by automating saving, treating it as a non-negotiable expense, and tracking it monthly. Tools like CogniFlow Books centralize your income, expenses, job costing, and cash flow so you can see your real monthly burn and track your runway — not guess at it.

Step 1: Know Your Monthly Operating Number

Pull the last 3–6 months of business activity and calculate your honest average monthly burn: rent, payroll (including yourself), utilities, software, insurance, loan payments, fuel, marketing. Focus on the baseline — what hits every month regardless of revenue.

You may find this number is higher than you thought. That's normal — and exactly why you need to see it clearly. With CogniFlow Books, expenses are categorized and summarized by month automatically so your true ongoing burn is visible at a glance instead of assembled from memory.

Step 2: Automate Paying Your Reserve First

You're not going to randomly wake up with a 3–6 month reserve. It has to be built intentionally. Treat it like a bill that gets paid before anything else.

Fixed percentage of revenue

5–10% of every month's gross automatically moves to a separate reserve account. Slow month? Smaller transfer. Good month? Reserve grows faster.

Fixed monthly amount

A set transfer every month until you hit your target. Works well if revenue is stable.

Hybrid approach

A minimum fixed amount every month plus extra on high-revenue months.

The transfer must go to a separate account— ideally a high-yield business savings or money market account with FDIC coverage and quick access. Not mixed into your operating account where it's easy to mentally spend.

Step 3: Protect the Reserve From Death by a Thousand Cuts

Your reserve has one job: protect the business from real shocks. Not every minor inconvenience.

Good reasons to use it

- ✓ Sudden revenue drop from losing a major client

- ✓ A broad economic hit or market slowdown

- ✓ Mission-critical equipment failure

- ✓ Brief cash gap from delayed receivables

- ✓ A clear, numbers-backed growth opportunity

Bad reasons to use it

- ✗ You overspent on discretionary stuff

- ✗ You hired too early without a plan

- ✗ You underpriced your core offers

- ✗ Funding personal lifestyle the business can't sustain

Whenever you tap the reserve: write down why you used it, decide how you'll rebuild it, and adjust your habits so the same problem doesn't repeat. CogniFlow Books shows your reserve trend alongside cash flow and expenses so you're never flying blind.

Step 4: Put Cash on a Dashboard and Watch It Monthly

At least once a month, review:

- • Current cash balance (operating + reserve)

- • Reserve amount and how many months of expenses it represents

- • Expected cash inflows (invoices, subscriptions, projects)

- • Expected cash outflows (payroll, rent, major bills, taxes)

- • Any upcoming large hits (equipment, renewals, tax deadlines)

What you watch, you manage. What you ignore, manages you. CogniFlow Books can automatically categorize transactions, generate real-time cash flow projections, and flag when reserves drop below your panic line — so you're not rebuilding a spreadsheet manually every month.

This Week: Exactly What You Should Do Next

Calculate your real monthly operating expenses

Pull the last 3–6 months and calculate an honest average. This is your burn rate. It's probably higher than you think.

Pick your panic line and target reserve

Decide how many months you want as a minimum (panic line) and a comfortable target. Write both numbers down.

Open a separate reserve account

A business high-yield savings or money market account with FDIC coverage and easy access. This is where your cushion lives — separate from operating cash.

Set up automatic monthly contributions

Choose a percentage or fixed amount you can realistically move every month — even if it's small — and automate it. Treat it like a bill.

Add cash and reserves to your monthly dashboard

Make your cash runway and reserve levels something you see every month — not once a year at tax time.

You don't have to hit your full reserve target this quarter. But if you commit to building it and protect the habit, you'll wake up one day and realize you're no longer one bad month away from panic — you're running a business on a foundation that can actually support the growth you're chasing.

See Your Real Cash Runway in CogniFlow Books

Cash flow forecasting, expense categorization, AR aging, and job profitability — all in one platform so you always know exactly where you stand. Try it free for 7 days.

Start Free Trial