You want the business to throw off real money — not “busy but broke,” not “just covering the bills,” but actual owner profit and wealth. You want to see seven figures in annual revenue and have something meaningful left over.

Here's the problem: nobody ever taught you how to think financially as a business owner.

You learned how to deliver your service. You learned how to sell. You learned how to grind. But nobody sat you down and walked through what profit really is, how cash flow really works, how to use debt without letting it use you, or how to read your own numbers well enough to scale without guessing.

This is the financial literacy you actually need if you want to build a business that can grow to seven figures and stay alive when things get bumpy.

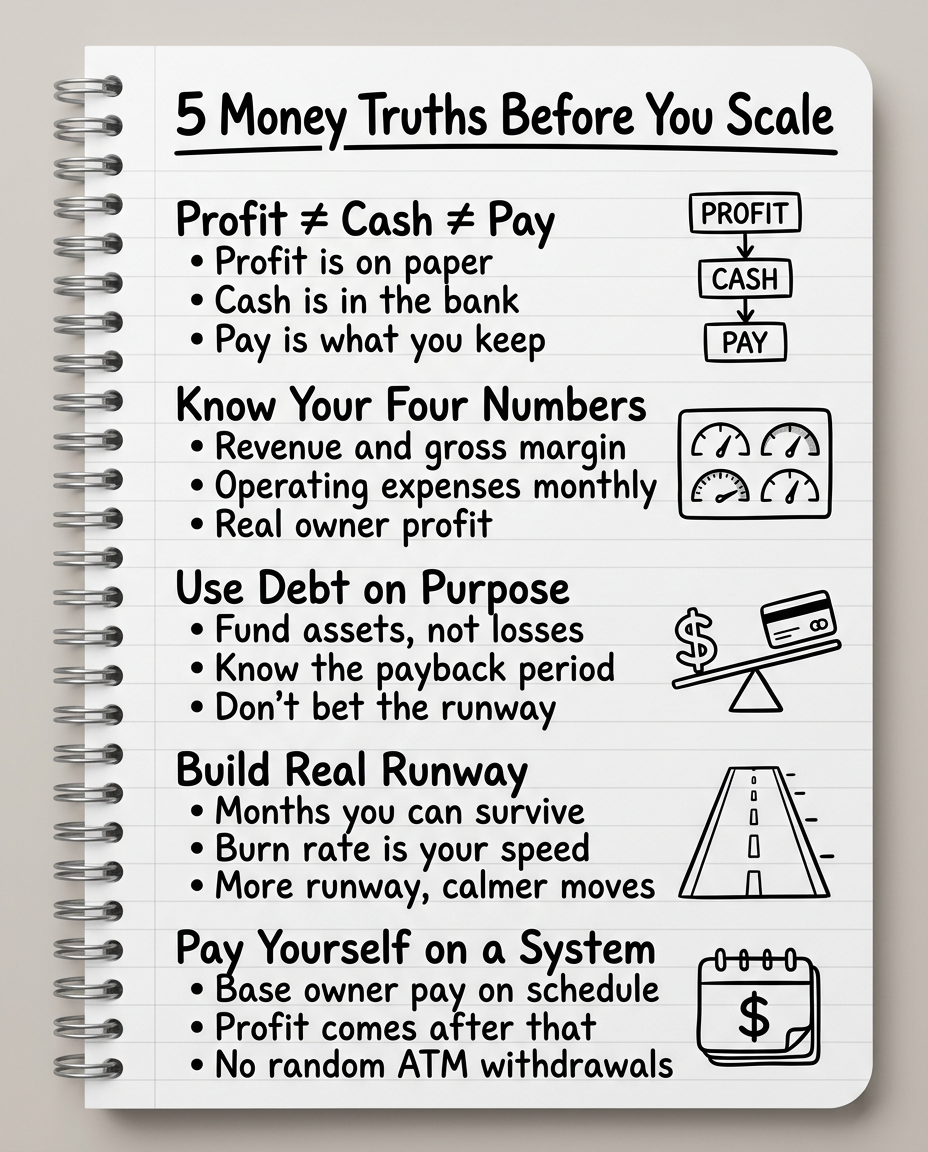

Profit, Cash, and Owner Pay Are Three Different Things

The first mental shift is simple, and almost everyone gets it wrong at first:

- Profit is what's left on paper after revenue minus expenses.

- Cash is what's actually in your accounts.

- Owner pay is what you take home.

They are related. They are not the same.

You can show a profit on your P&L and still have no cash because:

- Customers haven't paid yet.

- You're sitting on inventory or work in progress.

- You made big loan or tax payments that don't show up as “expenses.”

You can also have decent cash for a moment and still be unprofitable because you're burning through a line of credit, PayPal balance, or delayed bills.

Scaling to seven figures requires that you stop using your bank balance as your main financial indicator. Profit tells you if the business model works. Cash tells you how much runway you have. Owner pay tells you whether the business is feeding your life or using it.

Action Step

For last month, write down three numbers on one page: net profit, ending cash balance in your operating account, and what you actually paid yourself. Seeing them side by side will tell you more than any single report.

The Four Numbers That Drive a Seven-Figure Business

Forget the 50-line P&L for a second. When you're aiming for seven figures, you need a tight mental model built on four numbers:

- Top-Line Revenue — How much money came in.

- Gross Margin — Revenue minus direct costs tied to delivery.

- Operating Expenses (Opex) — What it costs to run the business before owner pay.

- Owner Profit — What's left after Opex and a fair market wage for your role.

If you can't say, roughly, what those four numbers are for the last 3–6 months, you're scaling blind.

Gross margin is the one almost everyone skips. If you do $1,000,000 in revenue and your direct costs (labor, materials, contractors, fulfillment) are $700,000, your gross margin is $300,000. That $300,000 is what you have left to fund operations, growth, and owner profit.

A “million-dollar business” with a 25% gross margin is a different animal than one with a 60% gross margin. The first might feel big and still leave you stressed. The second has room to hire, advertise, and build systems.

Action Step

Take your last full year and ballpark these four numbers. You don't need perfection — you need a clear sense of how much of your revenue you actually keep after delivering the work.

The Only Way to Think About Debt While You're Scaling

Debt is not automatically bad. It's also not automatically smart. The right way to think about business debt is simple:

- Good debt: financing an asset or capability that reliably increases your earning power (equipment that produces billable work, marketing that has a measurable return, systems that replace manual labor).

- Bad debt: covering persistent operating losses, plugging “we don't know where the money went,” or funding lifestyle you can't afford yet.

If your business is truly profitable and you use debt to accelerate something that already works, that can be a rational move. If your business is not profitable and you use debt to keep it on life support, you're just turning a business problem into a personal one.

Before you take on or extend any debt while scaling, you need to be able to answer three questions clearly:

- What specific revenue or cost savings will this allow me to create?

- What's the payback period — how long before the investment returns at least what it cost?

- If the upside takes twice as long as I think, can the business still service this debt without choking?

If you can't answer those, you're not making a strategic move — you're gambling.

Action Step

List every business debt or financing product you have (cards, lines, equipment, advances). For each, write: current balance, monthly payment, interest rate, and what it actually funded. If you can't name what it funded, that's a red flag.

Cash Runway: How Long Can the Business Breathe?

You can't scale if you're always one bad month away from panic.

Runway is how many months your business can operate at current spending levels if revenue dropped to zero. For an actively growing business, the exact number will move, but the habit of tracking it is non-negotiable.

To build your runway number:

- Calculate your average monthly burn (total cash out for the last 3–6 months).

- Look at your operating and reserve balances (not tax money).

- Divide balances by burn.

If your runway is under one month, you are in constant danger. Two to three months is survivable but stressful. Three to six months gives you room to fix problems, test new offers, and make bigger moves without every decision feeling life-or-death.

Scaling with no runway is like trying to climb higher on a ladder that's missing rungs. You might get up a bit, but any slip is catastrophic.

Action Step

This week, run the numbers and write your current runway in big digits somewhere you see daily. It changes how you think.

How to Pay Yourself Without Starving the Business

When you're pushing for growth, it's easy to swing between two extremes:

- Starving yourself: you pay yourself last (or not at all), telling yourself “it's for the business.”

- Starving the business: you take out whatever's left in the account whenever you feel like it, leaving the business short.

The financially literate way is to separate owner wages from owner profit:

- Owner wages: what the business pays you for the role you perform (sales, delivery, leadership). This should be consistent and budgeted, even if it starts modest.

- Owner profit: what you take as a distribution after the business has covered its needs and set aside reserves.

When you treat your draw like a random ATM, you never know if the business is actually profitable or if you're stripping it bare. When you treat yourself like an employee first and an owner second, you can see whether the business model really works.

Action Step

Decide on a base monthly owner pay that's realistic. Put it on a schedule. Stop taking random extra draws outside of planned profit distributions.

The Literacy Shift: From “Can I Afford This?” to “Does This Move the Model?”

Financially illiterate owners ask: “Can I afford this?” and look at their bank balance.

Financially literate owners ask:

- How does this affect my gross margin?

- How does this affect my runway?

- Does this strengthen or weaken my ability to generate profit next quarter?

- What has to be true for this to pay off?

Scaling to seven figures is not about finding one magic tactic. It's about stacking a series of financially sound decisions, month after month, while you see what's happening clearly enough to correct course.

That's what real financial literacy looks like for a business owner — not memorizing jargon, but understanding your own numbers well enough to use them as tools.

What to Do This Week

Calculate last month's net profit, ending cash, and owner pay on one page and look at the gap.

Ballpark last year's revenue, gross margin, operating expenses, and owner profit — even roughly.

List every debt product and what it actually funded; start a plan to eliminate anything that isn't clearly tied to earning power.

Compute your current runway in months and write it where you see it every day.

Decide on a realistic base owner pay and put it on a schedule instead of random draws.

See Your Numbers Clearly

If you want one place where you can see cash, invoices, job-level margins, and simple owner metrics at a glance — without building your own spreadsheet maze — that's what CogniFlow Books is designed for.

Start Free Trial7-day free trial · No accounting knowledge needed